Saving and risk profile

Now you can choose the level of risk you want to have.

The higher the risk level, the higher the expected return, but correspondingly, the risk is greater.

If you do nothing, you will remain at ‘miðal’. We have solid experience and can advise you on all pension-related questions

Choose your risk profile

Everyone needs to save for their pension, and now you can choose the level of risk you want to have.

You can choose from five different risk levels. They range from low risk to high risk, and you can always change the risk level at no cost. The default is that all customers start with a ‘Medium’ risk level.

In general, the more riskier investments, such as shares, fluctuate the most in value, but over time, shares provide higher returns. Bonds fluctuate less because the risk is lower, offering more stability in the investment portfolio.

Whether the risk is high or low is related to whether the money is invested in shares or bonds. If you mix both shares and bonds, the allocation between them determines the risk.

Choose a risk level that suits you.

What do I need to do?

Contact us if you want to change to a different risk level, or if you want to learn more about your options. You can also choose a risk level that suits you and submit the form to us.

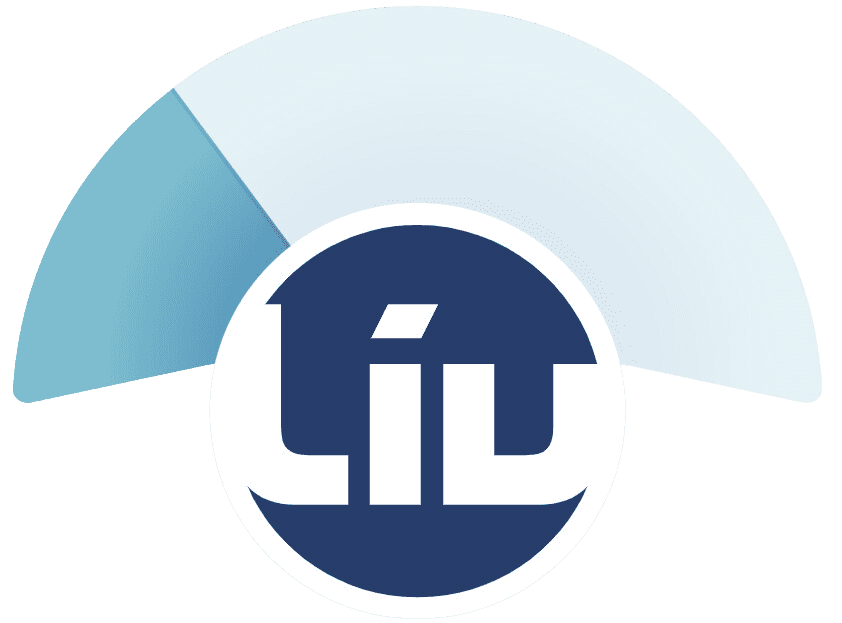

Low

It will be based on the fact that the saved value will be allocated to investments in the following way

55% bonds

45% shares and alternative investments

The profile has a relatively large proportion of bonds. The profile has limited risk, but also expects lower returns. When there are 15 years left until the pension is paid out, the investment risk decreases annually.

Medium

It will be based on the fact that the saved value will be allocated to investments in the following way

23% bonds

77% shares and alternative investments

The profile is between ‘Varið’ and ‘Høgt’ risk levels. Therefore, the expected return and risk are also between those mentioned profiles. When there are 15 years left until the pension is paid out, the investment risk decreases annually.

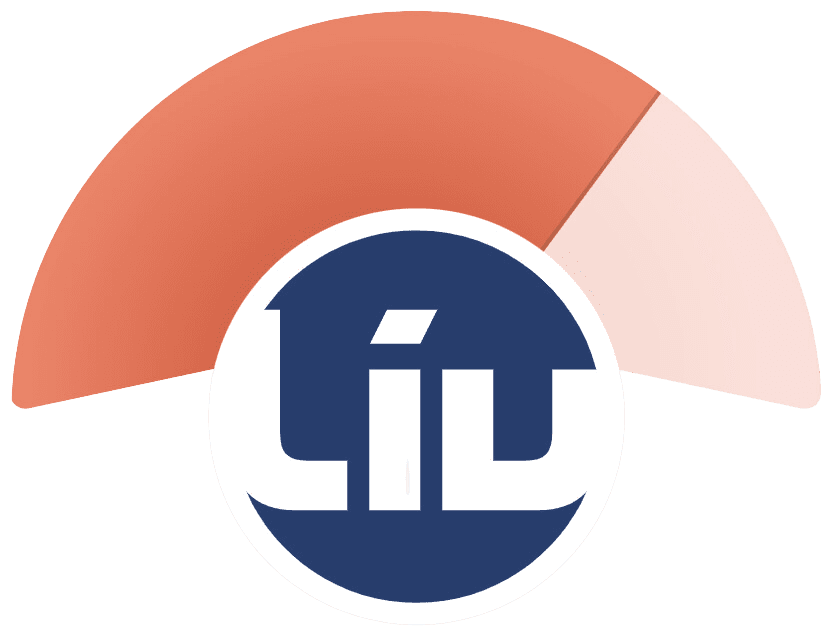

High

It will be based on the fact that the saved value will be allocated to investments in the following way

15% bonds

85% shares and alternative investments

The profile has the largest proportion of shares and other investments. The profile has a high expected return, but also a high level of risk. When there are 15 years left until the pension is paid out, the investment risk decreases annually.

Shares

It will be based on the fact that the saved value will be allocated to investments in the following way

100% shares

The profile only has shares and other investments. Therefore, the profile has the highest expected return, but correspondingly also the highest risk. The risk does not decrease, regardless of how many years are left until the payout

ESG

It will be based on the fact that the saved value will be allocated to investments in the following way

40% bonds

60% shares

The investment strategy has a composition of bonds and shares, where all investments are based on an ESG (Environmental, Social, and Governance) approach. This means that the investments support environmental, social, and governance sustainability issues. When there are 15 years left until retirement age, the investment risk decreases annually.

The risk decreases as retirement age approaches.

The risk will decrease 15 years before retirement age. The proportion of shares decreases annually to reduce the risk as you approach retirement age, and the proportion of bonds increases accordingly.

The risk with 100% shares does not decrease as you approach retirement age

How is the pension disbursed?

Contributions up to and including 31/12-2011

Accumulated savings and interest from the contributions during this period will be paid out in accordance with the provisions of the Interest Insurance Law.

Fees/taxes will be deducted in connection with the payout.

Contributions from 01/01-2012 to and including 31/12-2013

Accumulated savings and interest from the contributions during this period will be paid out in accordance with the provisions of the Interest Insurance Law

Contributions from 01/01-2014 to the present

Accumulated savings and interest from the contributions during this period will be paid out in accordance with the provisions of the Pension Law. The payout may be structured as shown below.

The payout is tax-free.

Lump-sum payout

At most, 15% of the accumulated pension can be paid out at once.

Installment payment

At most, 55% of the accumulated pension can be paid out as a Defined Benefit Pension, which will be paid in equal monthly installments over a period of at least 10 years

Life Annuity

At least 45% of the accumulated pension must be paid out as a Life Annuity. The payout will be made monthly, starting when you turn 67, and will continue for as long as you live.

Payout in case of death during the contribution period

The accumulated value will be paid out to the next beneficiary, unless another written agreement is made with LÍV.

We are ready to help you

If you have questions or would like advice, you are welcome to contact us.

Send us an email on liv@liv.fo, call us at +298 31 11 11, or log in to the customer portal

Mítt LÍV and send us a message